We’re all wired differently. Our passions, our fears and our dreams are different. And when we hear the word money, we all have unique thoughts and emotions too.

For years now, I’ve been coaching people about personal finance. What I’ve come to learn time and time again, family after family, is this: Whether or not you’re successful with money isn’t about knowledge, IQ or how good you are at math. It’s about behavior.

My dad, Dave Ramsey, has been saying it too: “Personal finance is 80 percent behavior and only 20 percent head knowledge.” That’s why our proven plan for getting out of debt relies on changing your behavior, not throwing a bunch of numbers and formulas at you.

You see, money isn’t the problem. What you don’t know about yourself and why you do what you do is the problem.

Self-Awareness Is Key to Winning with Money

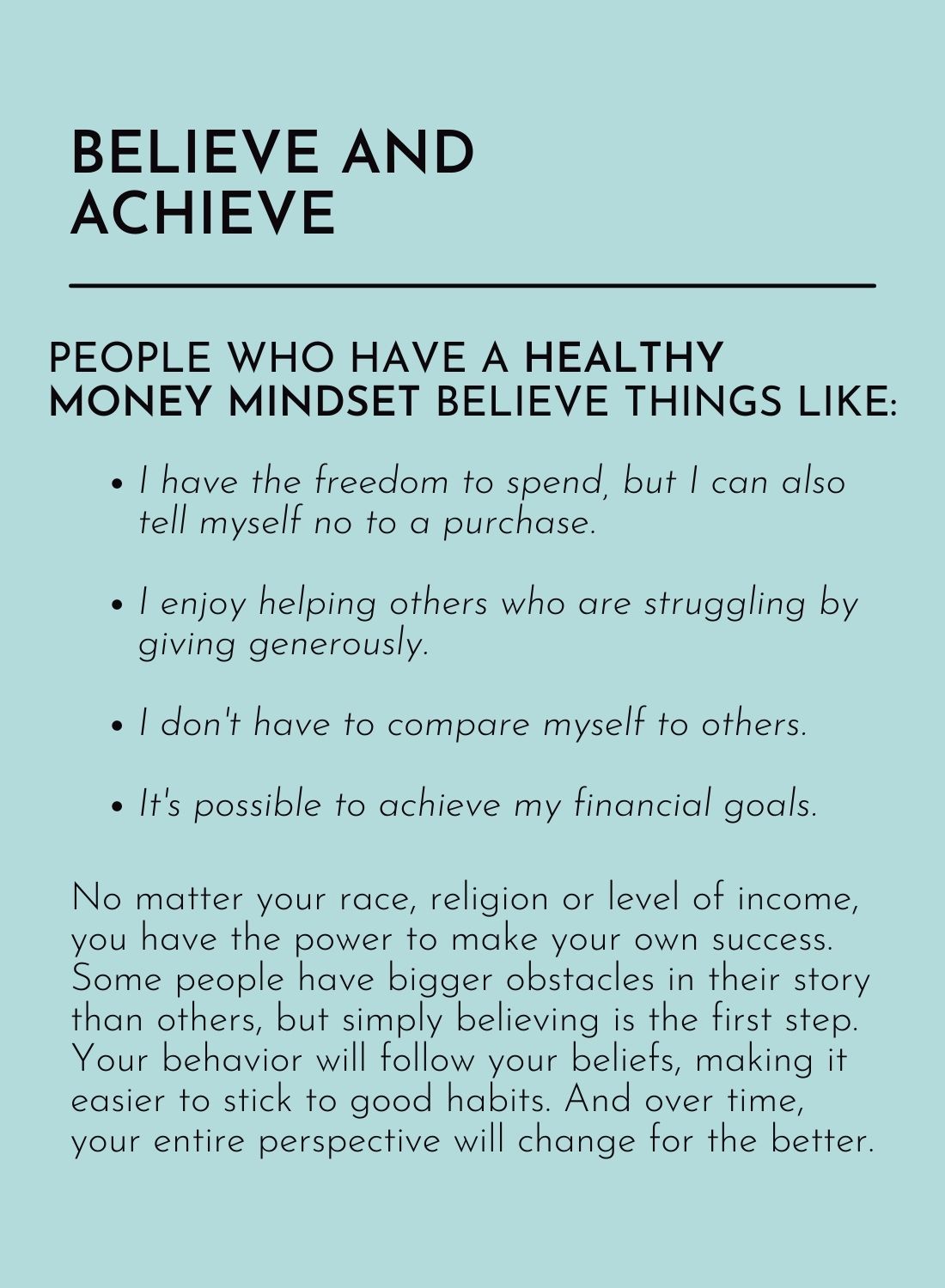

Once you know yourself better, you can harness the power of your own mind, your thoughts and your will—and you can make lasting change to be the healthiest version of you.

Right now, in Nashville where we live and through much of the South, the Enneagram is huge. It’s a personality typing system, and it’s honestly the best assessment I’ve found that accurately describes the way I tick.

The reason I love the Enneagram and other personality tests like it is because they give me the gift of self-awareness. Self-awareness is incredibly valuable. Socrates said, “The unexamined life is not worth living.” If we live our whole lives without learning which strengths, weaknesses, perceptions and tendencies we bring to the table, we’ll never grow. And we’ll never experience real transformation with our money, either.

Over the last decade, I’ve seen this stuff play out in real life while coaching people with their money. If you want to get to the root of why you behave the way you do—why you spend, save, use debt and more—you’ve got to learn about the mindset behind the way you view money.

5 Ways Your Mindset Affects Your Money

I love digging into money tendencies and how they play into someone’s story. Like I said before, everyone is different, and none of these tendencies are right or wrong. It’s just how you’re naturally wired.

1. Spender vs. Saver

You can probably identify whether you’re a spender or a saver pretty easily. Spenders see nothing but possibilities when it comes to money! This one is totally me. I’m a spender, so whenever I have extra money, it burns a hole in my pocket, and I can’t wait to spend it.

But a saver’s first instinct is to not spend their money. Savers actually enjoy tucking money away because it makes them feel good. Savers tend to be more patient people and are willing to wait to make a purchase.

What’s dangerous for both spenders and savers is going to the extremes. As a spender, if you spend everything you make, you’ll wind up broke. And savers, if you save everything you make, you’re going to miss out on a lot of fun experiences that make life joyful.

2. Nerds vs. Free Spirits

Nerds get excited about telling their money where to go each month. They thrive on crunching numbers and genuinely look forward to organizing their budget. They might use spreadsheets, apps and research to find ways to make their money go further. Everything has a nice, neat place, and they love it.

Free spirits are where the party’s at. They don’t get too bogged down in the details, and they find it easier to just sit back and enjoy life. Thinking about the budget might make a free spirit break out in hives. However, the shopping and entertainment categories are basically their love language.

Free spirits need the nerds to help them make a realistic budget. My husband, Winston, is a nerd, and I love his attention to detail and how he always knows exactly what’s going on. And hey, free spirits can learn to love budgeting too! A budget gives you permission to spend.

Nerds need the free spirits to inject some fun money into the budget for nonessential categories, like date nights, vacations and birthday parties.

Before you assume people who like to save money are the nerds, and people who love spending are the free spirits, guess again. My dad is actually a nerd-spender. He loves spending money, but he also loves playing with numbers and having control over the budget.

3. Safety vs. Status

Are you financially motivated by safety or status? For this one, you may have to do some real soul-searching. Think through what motivates you when you spend or save. And be honest with yourself! This tendency is key to understanding why you handle money the way you do.

People who value safety want the security that money can bring. They want to know they can withstand job loss, a medical emergency or even just a dip in income. If you’re a safety person, you need to watch out for living in fear because fear can keep you from giving generously, investing in retirement, or even spending money on a new pair of shoes when the ones you wear every day have a hole in them and clearly need to be replaced.

If you recognize the unhealthy side of the safety tendency in yourself, the best thing you can do is build up an emergency fund. That way, you know you have money set aside for when the unexpected happens, and you can still hold your money with an open hand for the other things you want to do with it.

If money is about status for someone, it’s how they measure success. The amount of money they have affects the type of home they live in, the activities they’re involved in, and their ability to go on that dream vacation. When someone prioritizes status in an unhealthy way, they’ll be more likely to go into debt to prove their status to others. (More on this motivation later.)

4. Abundance vs. Scarcity

People who live in an abundance mindset believe there’s always more than enough for everyone. They take more risks, and they don’t fear the outcome of a decision. They also tend to be natural givers, believing there are always ways to make more money.

This glass-half-full mentality can interfere with making wise choices with money. If this is you, seek the advice of family and friends you trust before making a big purchase (even if it’s for someone else). Don’t make important decisions in a vacuum.

People who operate under the assumption of scarcity make money decisions based on a belief that resources are finite. They hold onto possessions tightly because they “might need that someday.” And sometimes they fear losing things because they might not be able to replace them.

If you lean toward scarcity, don’t miss smart financial opportunities that will move you forward in life because fear is undermining your thinking. I always say that fear is a terrible financial advisor. Focus on facts, not fear, and you’ll feel better about your money.

5. Your Family and Childhood

The way you heard your parents talk about money—or not talk about it—definitely influenced your attitude about it from an early age. This alone won’t define your money mindset, but it’s good to be aware of.

Maybe you grew up in a family where money was a source of conflict. It was something that brought tension into your household, and you felt the stress around your parents struggling to pay their bills. That definitely impacts your view of money today!

Or maybe you grew up in a household where you didn’t see or hear about money. So now, as an adult, you’re tempted to not manage your money at all. Some say ignorance is bliss, but that’s not true when it comes to your money. It’s like a boat with no captain. You need to pay attention to where the boat is going. Someone has to steer it. If you don’t tell your money where to go, you’ll wonder where it went.

This is where knowing yourself can lead to healing, change and more progress than you’ve seen before.

How Your Money Tendencies Affect Your Decisions

The truth is that money is just a magnifying glass—it makes you more of who you are. If you’re kind and generous, you’ll be even more kind and generous with money. If you’re rude and self-centered, you’ll be even more rude and self-centered with money. Money is simply a tool, and you get to determine what to do with it.

Think of money like a brick—it doesn’t have feelings or motives. But someone can use a brick to throw it through a window to rob a store. Or someone could use it to build an orphanage. It can be used for good or evil. The same is true of money.

Your feelings and motivations around money influence the way you use it. One example for me is in the safety versus status tendency. I’m naturally motivated by status when it comes to my money. I’m more likely to value a name-brand purse or luxury vacation, and I’m more likely to find a way to justify a larger purchase if, on some level, it makes me feel successful.

On one hand, this just means I like nice things—and please hear me when I say there’s nothing wrong with having nice things if you can afford them. But knowing that I have that status tendency means I have to keep my spending in check. Now, before I make a purchase, I always ask myself, “Would I still buy this if no one else ever saw it?”

Remember that the biggest obstacle between where you are today and becoming wealthy is not opportunity or income—it’s you controlling you. So, put your focus on the things you can control: your thoughts and your habits. It takes dedication and discipline, but the good news is, it doesn’t cost a thing.

Know Yourself, Know Your Money

The New Book by Rachel Cruze

I know this stuff is hard work, but I also know that you can do it. I know you can, because I’ve seen millions of people from all backgrounds and income levels find the courage to make lasting change—not just for them, but for their whole family tree!

That’s what inspired me to write my new book, Know Yourself, Know Your Money: Discover WHY you handle money the way you do, and WHAT to do about it. It will help you examine your own everyday tendencies with money, make lasting change in your habits and behavior, and get on the fast track to achieving your dreams.

Leadership speaker Charles Jones once said, “You’ll be the same person in a year as you are today except for the people you meet and the books you read.” Here are some more of my favorite books for changing your mindset:

- The Total Money Makeover by Dave Ramsey

- Switch On Your Brain by Dr. Caroline Leaf

- The Power of Habit by Charles Duhigg

- The 7 Habits of Highly Effective People by Stephen R. Covey

This article originally appeared in the March/April 2021 issue of SUCCESS magazine.

Photo courtesy of Ramsey Solutions